.avif)

%20(5).avif)

If you’re working to improve your credit score so you can buy a house in 2025, you’ve probably asked: “Should I pay this old collection or charge-off?” It seems logical—clean up your debt, boost your credit, qualify for a mortgage.

But here’s the surprising truth: Paying off certain debts can actually hurt your credit score—if done the wrong way.

In this guide, we’ll break down exactly when it makes sense to pay—and when it doesn’t—so you can take the right steps toward homeownership.

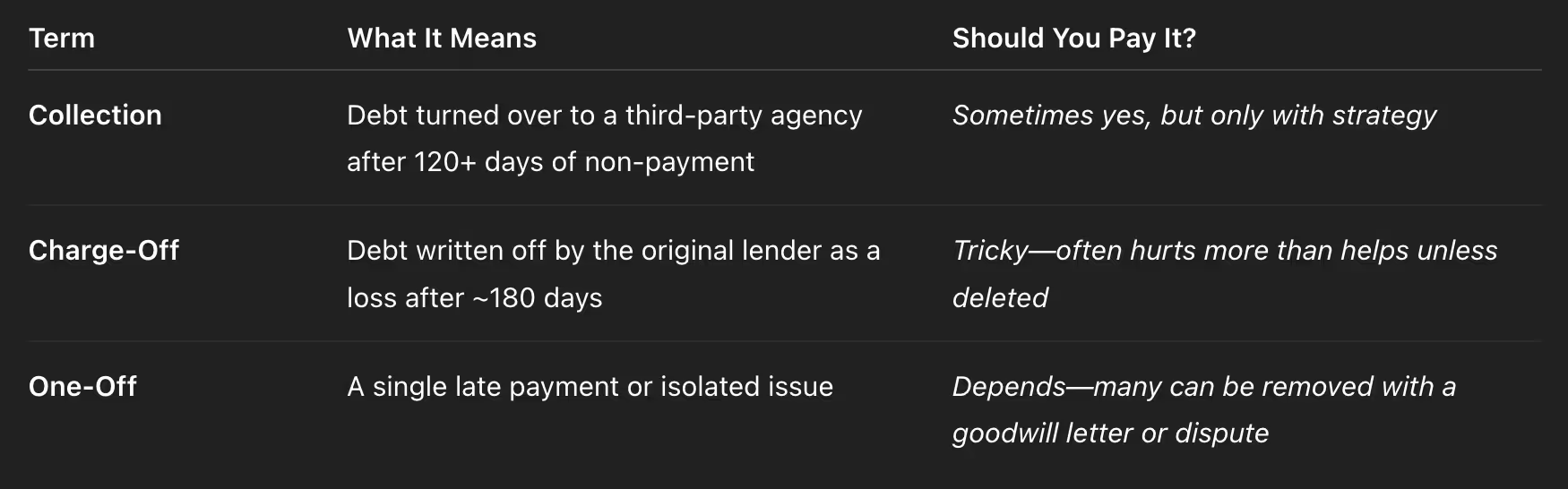

What’s the Difference Between Collections, Charge-Offs & One-Offs?

When it comes to improving your credit score before buying a home, not all debts are created equal. Below is a breakdown of three common negative credit items—collections, charge-offs, and one-offs—and whether paying them off is a smart move or a potential mistake.

Part 1: Collections – What They Are & When to Pay

What Is a Collection?

A collection happens when a bill goes unpaid for 120 to 180 days and is handed over to a third-party debt collector. These can include:

- Medical bills

- Credit cards

- Utility bills

- Personal loans

Should You Pay Off a Collection Before Buying a Home?

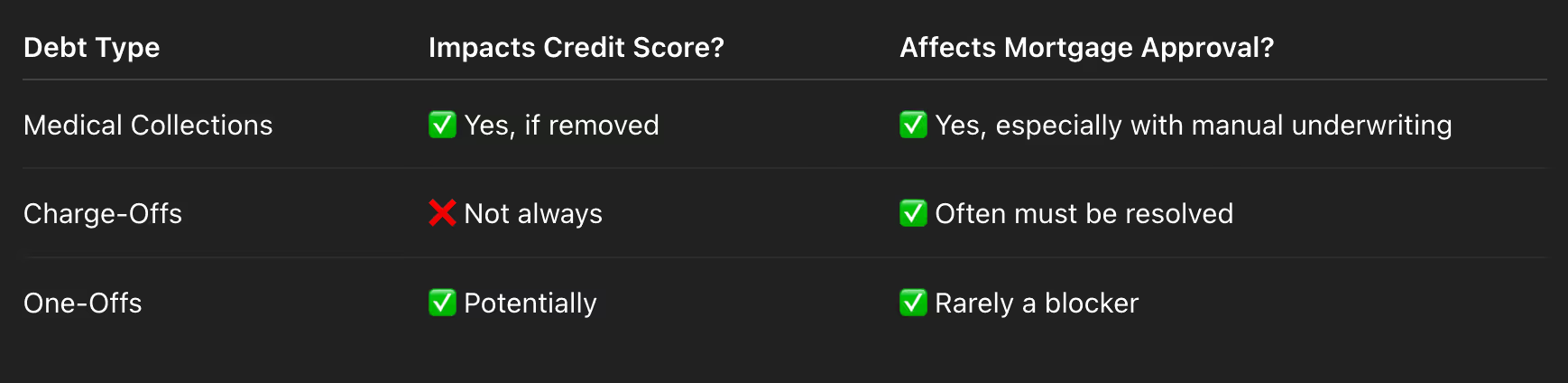

✔️ Medical Collections (2021 Medical Debt Relief Act)

- Paid medical collections are removed from your credit report

- Even if they don’t impact your mortgage DTI, they can boost your score

- Pro Tip: Settle and get documentation—it’s worth it

✔️ Pay-for-Delete Collections

Some collection agencies may remove the account from your credit report in exchange for payment. This is called Pay-for-Delete.

- Always ask in writing first (get a Letter of Deletion)

- Only pay if deletion is confirmed

⚠️ Collections That Won’t Be Deleted

Paying can update the Date of Last Activity (DLA) and make the account look newer—lowering your score temporarily. It also resets the 7-year reporting clock.

❌ Government Debts

Student loans, child support, or IRS debt may not improve your score when paid—but often must be settled to qualify for a mortgage.

Bottom Line for Collections:

Don’t pay a collection until you understand how it will impact your score.

Our team helps you navigate when to negotiate, when to hold off, and when to settle.

Part 2: Charge-Offs – Understand the Risks Before You Pay

What Is a Charge-Off?

A charge-off happens when the original creditor gives up on collecting your debt after ~180 days of non-payment and marks it as a loss. But the debt doesn’t disappear—it still affects your credit and may be sold to collections.

Should You Pay Off a Charge-Off?

📉 Paying Doesn’t Always Help Your Score

Unless the creditor agrees to delete the account, paying it only updates the DLA—which can lower your score short-term.

💳 Credit Cards (< 2 Years Old)

These hurt the most due to both missed payments and high utilization. Paying off a recent charge-off may help—but older accounts require strategy.

🚗 Auto Loans & Personal Loans

Affects only payment history, not utilization. If it won’t improve your score (or get deleted), paying may not be worth it.

🎓 Private Student Loans

Private (not federal) loans can be charged off. Some lenders may require payment before loan approval—especially if recent.

Bottom Line for Charge-Offs:

Paying a charge-off may help with loan approval—but not necessarily your score.

Let us help you decide if paying is the right move, or if there’s a better path forward.

Part 3: One-Offs – How to Handle Small Credit Blemishes

What Are One-Offs?

These are isolated incidents—a single late payment, a small collection, or a one-time financial mistake.

Should You Pay or Dispute?

- Dispute If Inaccurate: Wrong date? Not your account? Dispute it with the credit bureaus.

- Goodwill Letter: Been a loyal customer? Ask the creditor to remove it as a favor.

- Don’t Panic: One mistake won’t ruin your credit. Focus on consistent, healthy credit habits.

Bottom Line for One-Offs:

These are often fixable. We’ll help you evaluate the best way to respond and move forward.

How Paying Off Debt Affects Mortgage Approval in 2025

Need Help Reviewing a Credit Report? Let’s Talk Strategy.

Trying to DIY your way through credit repair before buying a home?

We’ve seen it backfire—too many times.

Before you pay that old debt:

✔️ Let us pull a soft credit report

✔️ Review your unique situation

✔️ Create a smart plan that boosts approval odds AND keeps your score healthy

📲 Start here → www.TheSherryRianoTeam.com

We’re here to help you get mortgage-ready the smart way.

Frequently Asked Questions (FAQ)

Q: Will paying off a collection instantly raise my credit score?

A: Not always. If the account stays on your report and updates the Date of Last Activity, it can actually lower your score temporarily.

Q: What is a “pay-for-delete” deal?

A: This is when a collection agency agrees to delete the account from your credit report after payment. Always get it in writing before paying.

Q: Do charge-offs need to be paid before buying a house?

A: It depends on the lender, the amount, and the age of the account. Some lenders require it, others don’t.

Q: What’s the difference between a charge-off and a collection?

A: A charge-off is marked by the original creditor. A collection is when the debt is sold to a third-party collector.

Q: How long do collections and charge-offs stay on my credit report?

A: Up to 7 years from the Date of First Delinquency. But paying them can reset that timeline—so timing matters.

Let’s Get You Closer to Homeownership

Whether you're ready to apply now or need a few months to prep, we’ll guide you every step of the way.

Because financial strategy shouldn’t be guesswork—and with the right partner, it isn’t.

.png)

.png)

.png)