.avif)

.avif)

If you're buying a condo, selling one, or already living in one with a mortgage, there are some important changes coming that your lender should already be talking to you about.

Fannie Mae released Lender Letter LL-2026-03, which updates the rules around how condo projects get approved for financing and how property insurance works. Most of it goes into effect before the end of 2027, and some of it is already in effect right now.

This isn't inside-baseball lender stuff. These changes affect real buyers, real HOA dues, and real insurance policies.

Here's what you need to know.

What Is Fannie Mae and Why Does It Matter for Your Mortgage?

Fannie Mae is a government-backed entity that buys mortgages from lenders after they close. When Fannie Mae sets guidelines, lenders follow them, because if a loan doesn't meet Fannie Mae's standards, the lender can't sell it on the secondary market.

That means Fannie Mae's rules directly affect whether or not you can get a loan on a specific property. And for condos specifically, the project itself has to meet Fannie Mae's requirements - not just you as a borrower.

This is why condo financing can feel more complicated than buying a single-family home. You're not just qualifying yourself. The condo association has to qualify too.

The 3 Big Changes From Fannie Mae LL-2026-03

Change #1: Condo Projects Now Face Tougher Financial and Safety Requirements

What's changing: Fannie Mae is tightening the standards condo associations must meet before a loan can be approved on a unit within that building.

The two most important updates:

Higher reserve fund requirements (effective January 4, 2027)

Condo associations will be required to set aside at least 15% of their annual budget into a reserve fund - money earmarked for future repairs and capital improvements. The current requirement is 10%.

This might sound like a minor percentage change. It isn't. For associations already running lean budgets, this could mean HOA dues going up in 2026 or 2027 as boards work to meet compliance. And for buyers shopping condos right now? This is a question worth asking the listing agent before you fall in love with a unit.

Limited reviews are going away (effective August 3, 2026)

Right now, lenders can use a "limited review" shortcut to approve certain condo loans faster. It's a lighter-touch process that doesn't require pulling all of a condo association's financial records and meeting minutes.

Starting August 3, 2026, that shortcut is largely eliminated. Most condo projects will require a full review - meaning the lender has to collect and analyze the association's financials, budget, insurance, and any deferred maintenance or pending litigation before the loan can close.

What this means for buyers: timelines for condo purchases could get longer if the association's records aren't in order. And some buildings that were easy to finance before may become harder to finance after this date.

Florida exception: New condo projects in Florida will actually see slightly relaxed rules. Lenders will no longer need to submit Florida files to Fannie Mae for a special secondary review, which should streamline approvals in that market.

Change #2: Property Insurance Rules Are Getting Updated - in Both Directions

Fannie Mae made a series of insurance-related changes that go in two different directions: some are meant to give homeowners flexibility as insurance costs have surged, and others are designed to make sure condo owners don't end up underinsured.

Flexible roof coverage (now in effect)

Previously, Fannie Mae typically required that roofs be insured for their full replacement cost. The new guidelines allow policies that cover roofs at "Actual Cash Value" - which is the depreciated value of the roof based on its age, not the full cost to replace it.

This matters because ACV policies are significantly cheaper. As insurance premiums have climbed nationally and in North Carolina, this change gives homeowners and condo associations more flexibility to find affordable coverage without violating their loan terms.

New limits on condo unit policy deductibles - HO-6 policies (now in effect)

If you own a condo, you carry a personal policy called an HO-6 that covers your individual unit. Fannie Mae now sets the maximum allowable deductible on your HO-6 at the greater of $2,500 or 5% of your coverage amount.

Why this matters: if your deductible is too high, your loan could be flagged during a future refinance or sale. Worth a quick review of your current policy if you already own a condo.

Master policy gap coverage requirement (now in effect)

Here's one that catches a lot of condo owners off guard.

Most condo buildings carry a master insurance policy that covers the exterior and common areas. But many of those master policies have what's called a "per-unit deductible" - meaning if there's damage, each affected unit owner is responsible for a portion of the deductible, sometimes up to $50,000.

Under the new guidelines, if a building's master policy has a per-unit deductible of up to $50,000, individual unit owners are now required to carry their own HO-6 policy to cover that gap. If you don't have it, your mortgage servicer could require you to get one.

Change #3: Annual Insurance Reminders Are Now Required

This one's simple. Your mortgage servicer - the company you send your monthly payment to - is now required to send you an annual reminder to review your insurance coverage.

The intent is to prevent homeowners from becoming underinsured as construction costs and replacement values climb. If you bought your condo five years ago and your coverage hasn't been updated, you may be insured for less than it would actually cost to rebuild or repair.

When you get that annual notice, don't ignore it. Take it as a cue to call your insurance agent and confirm your coverage limits are still accurate.

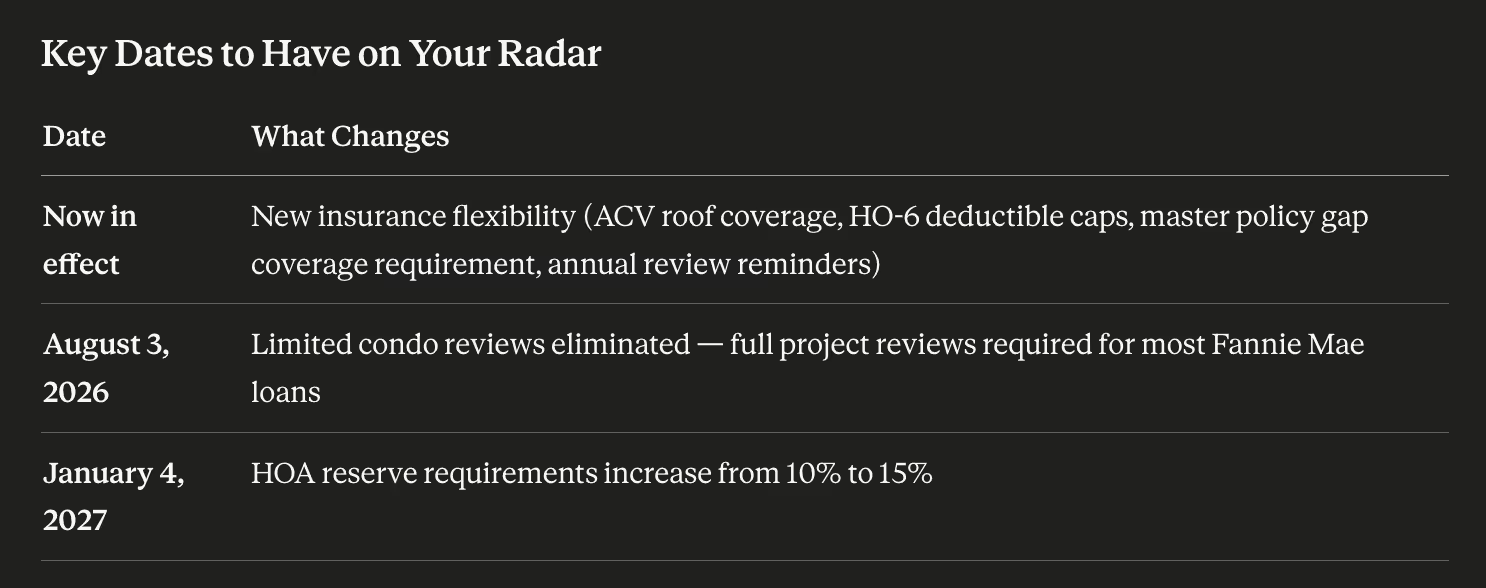

Key Dates to Have on Your Radar

Now in effect

New insurance flexibility (ACV roof coverage, HO-6 deductible caps, master policy gap coverage requirement, annual review reminders)

August 3, 2026

Limited condo reviews eliminated - full project reviews required for most Fannie Mae loans

January 4, 2027

HOA reserve requirements increase from 10% to 15%

What Condo Buyers Should Ask Before Going Under Contract

With these changes on the horizon, there are specific questions every condo buyer in North Carolina should be getting answered before they write an offer. Don't wait until you're under contract to find out the building has issues.

Ask these questions early:

1. Is this condo project already Fannie Mae approved? If yes, your lender can usually confirm that quickly. If not, a full condo questionnaire and review will be required before your loan can close - which adds time and introduces risk if the association's records are problematic.

2. What does the HOA's current reserve fund look like? Ask what percentage of the annual budget is currently set aside for reserves. If it's at 10% today and the new requirement is 15%, what is the board's plan? Are dues going up? Has there been a special assessment recently?

3. Does the HOA currently have pending litigation or deferred major repairs? Both of these are automatic flags in a full condo review. Roof replacements, structural repairs, and lawsuits can all create problems for financing.

4. What is the per-unit deductible on the building's master insurance policy? If it's close to $50,000, you'll need to make sure your HO-6 policy is in place to cover that gap at closing.

5. What does your personal HO-6 policy cover - and is the deductible within the new limits? If you're refinancing or if your existing policy has a high deductible, your lender may flag it under the new guidelines.

If You're Already in a Condo - Here's What to Review Now

You don't have to be in the middle of a transaction for these changes to matter. If you currently own a condo with a mortgage:

Pull out your HO-6 policy and check your deductible. Under the new guidelines, it should be no greater than $2,500 or 5% of your coverage amount, whichever is higher. If your deductible is higher than that, you may want to adjust before your next refinance.

Find out your building's master policy per-unit deductible. Your HOA board should be able to tell you this. If it's significant and you don't currently carry an HO-6 policy, your servicer may require you to get one.

Check whether your coverage has kept up with replacement costs. With construction and materials costs where they are today, a policy you set up three years ago may not be sufficient to fully rebuild or repair your unit.

Why Condo Financing Has Always Required Extra Attention

This is nothing new for experienced lenders, but it's worth saying plainly for buyers who are new to this: condo financing has always been more complex than financing a single-family home.

When you buy a condo, you're buying a slice of a collectively managed building. The financial health and physical condition of that entire building — not just your unit — affects your ability to get a loan. If the HOA is mismanaged, under-reserved, or dealing with deferred maintenance, it creates real risk for lenders.

These new Fannie Mae guidelines are responding to events that have made that risk more visible — including structural failures in aging condominium buildings. Lenders taking a harder look at condo associations before approving loans is genuinely good for buyers in the long run, even if it adds friction to some transactions.

The buyers and agents who get ahead of it — by asking the right questions before going under contract — will have a smoother experience than those who find out at underwriting.

How We Handle Condo Transactions at The Sherry Riano Team

At The Sherry Riano Team, condo review is part of our process before you ever apply. When a buyer comes to us interested in a condo, one of the first things we do is look at the project — because finding out a building has a problem after you're under contract is a much harder conversation than finding out before.

We've been doing this long enough to know which condo communities tend to sail through reviews and which ones need a closer look. And we know how to structure financing around the ones that present unique challenges — including non-warrantable condo options for projects that don't meet conventional guidelines.

If you're buying, selling, or financing a condo in Raleigh, Cary, Durham, Wake Forest, Clayton, or anywhere in the Triangle area, we'd love to take a look at the project early in your process.

Call or text us at 919-234-7415 or visit thesherryrianoteam.com to schedule a strategy call.

Frequently Asked Questions

Will these changes affect my current mortgage? Not directly — your existing loan terms won't change. However, if you refinance or sell, the condo project will need to meet the current guidelines at that time.

What is a non-warrantable condo? A non-warrantable condo is a project that doesn't meet Fannie Mae's or Freddie Mac's eligibility requirements for conventional financing. There are still loan options available for non-warrantable condos — they just involve different programs, usually at slightly different terms. We offer non-warrantable condo financing at The Sherry Riano Team.

How long does a full condo review take? It depends on how quickly the HOA responds to the condo questionnaire your lender sends. If the association is well-organized, it can be turned around in a few days. If they're slow or their records are disorganized, it can add one to two weeks to your closing timeline. Another reason to start early.

Can my HOA fail the Fannie Mae review? Yes. If an association has pending special assessments, significant deferred maintenance, active litigation, or doesn't meet reserve requirements, the project may be ineligible for conventional financing. This doesn't mean a unit in that building can't be financed — it may mean using a different loan type.

What is an HO-6 policy? An HO-6 is a personal homeowner's insurance policy for condo unit owners. It covers your personal belongings, the interior of your unit, and liability. It also fills the gap between what the building's master policy covers and what you're personally responsible for.

Ready to Talk Through Your Condo Purchase or Refinance?

These changes are moving fast - and the buyers and agents who get out ahead of them are going to have a much smoother experience than those who find out mid-transaction.

Whether you're just starting to shop, already under contract, or sitting in a condo you're thinking about refinancing, the best thing you can do right now is get a lender's eyes on the project early.

That's exactly what we do.

At The Sherry Riano Team, we don't wait for underwriting to surface problems. We review condo projects as part of our strategy-first process — before you ever fill out an application — so there are no surprises later.

Here's what a call with us looks like:

We talk through the property you're interested in, flag any potential project concerns early, walk you through loan options including conventional and non-warrantable condo programs, and make sure your insurance is set up correctly from day one.

No pressure. No application required to have the conversation.

Call or text us directly at 919-234-7415 or click here to schedule your strategy call.

We're based in Cary, NC and serve buyers and homeowners across the entire state of North Carolina.

The Sherry Riano Team | Developer's Mortgage Company (NMLS #225548) | Sherry Riano NMLS #71774 | Licensed in NC | Equal Housing Lender | This is not a commitment to make a loan.

.png)

.png)

.png)